Our Colby INNOVATION Portfolio is up 59% for

the first half of 2026, which is 521% better than the 10% gain for the S&P

500 index. In addition, our Bull/Bear Portfolio outperformed the S&P 500

Index by 64%, and our Fixed-Income Portfolio outperformed the S&P U.S.

Aggregate Bond Index by 91%. All of our clients have made positive returns over

the past 15 years while taking substantially less risk. We offer complete

transparency, anytime access to your funds, and low fees. Your assets are

secure, insured, and you keep control over your money. For details email info@colbyassetmanagement.com or call 646-652-6879.

Technology ETF (XLK)rose above its 50-day SMA on 8/4/2026, signaling a renewed bullish

uptrend. The main trend remains bullish as long as the 50-day SMA stays above

the 200-day SMA. Look for resistance near 182 and 198. Support sits around the recent

lows above 166 and 156-160. Fundamentally, there is no evidence of a slowdown

in demand for technology. Overinvestment concerns that have been persistent

since the June peaks appear to be easing following very strong earnings reports.

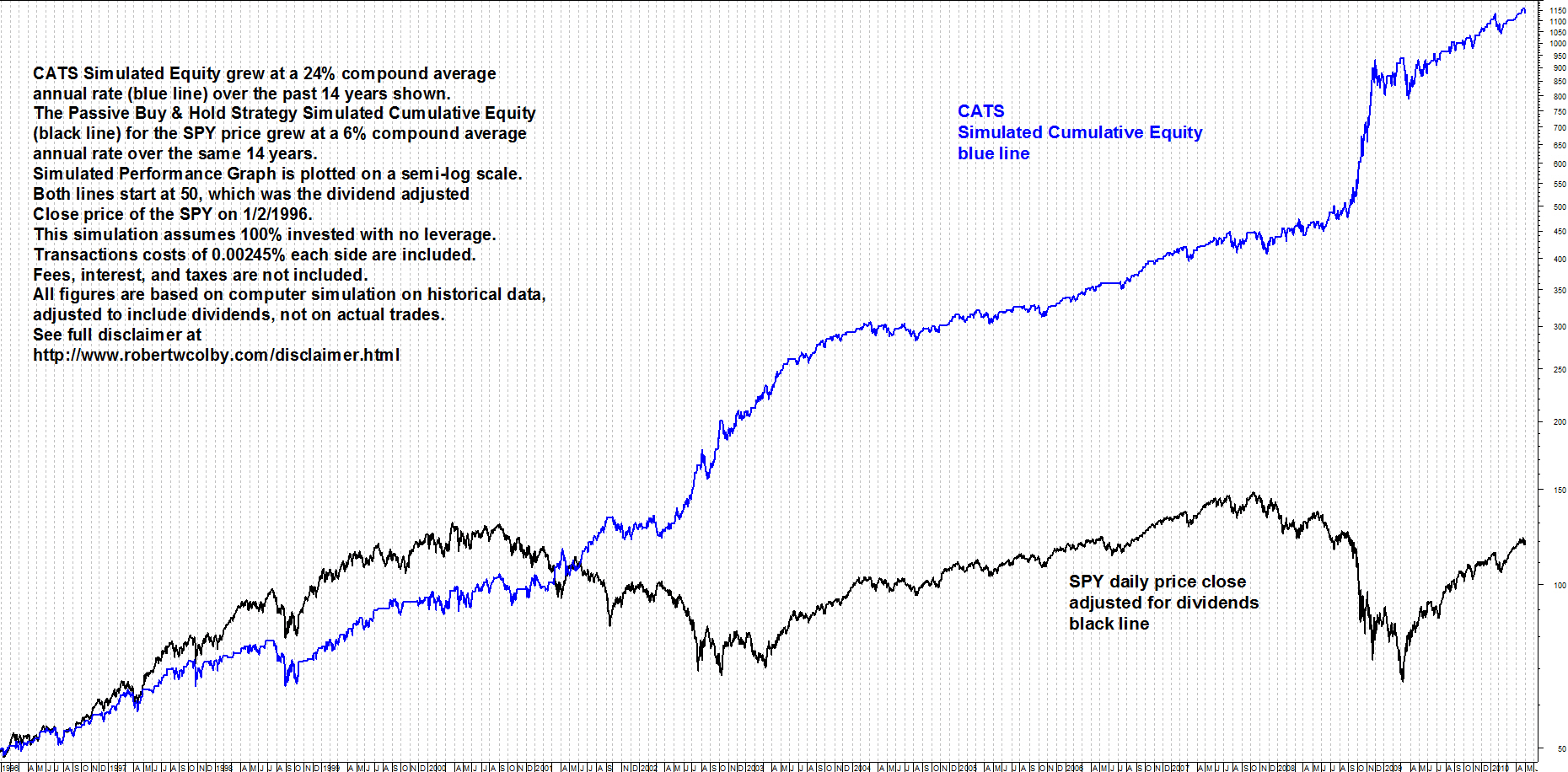

11-Year Outperformance by the Top 10 Exchange Traded Funds Weekly Rankings of Major Trend Relative Strength

My weekly Top 10 ETFs ranked by the Major Trend Relative Strength outperformed the S&P 500 over an 11-year period of real-time weekly tests. Click here for a graph of simulated performance.

My book was named one of the top investment books by Stock Trader's Almanac and also received an excellent review in Futures Magazine.

My ETF Rankings are not investment advice. Rather, they are an objective ongoing research study.

Analysis of market forces may offer a sense of probabilities. But the many variables that can impact market prices are notoriously difficult to predict. Sound trading tactics are always recommended. See my Money Management Rules.

According to CFTC Rule 4.41, hypothetical or simulated performance results have certain limitations. Unlike an actual performance record, simulated results do not represent actual trading. Also, since the trades have not been executed, the results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. No representation is being made that any account will or is likely to achieve profit or losses similar to those shown.

Trading and investing involve risk of significant loss. Your use of this site means that you have read, understood, and accepted my Disclaimer.

Robert W. Colby, CMT is a consultant to institutional and private investors and traders, providing regular analytical reports, custom research services, and trading systems tailored to clients' objectives. Clients include the most successful traders and investors in the world. Robert is the author of The Encyclopedia of Technical Market Indicators, which is the standard reference for indicator and trading systems design. Previously, at several large Wall Street firms, Robert worked as a proprietary trader, technical analyst, and fundamental analyst. He also was adjunct professor at New York University and New York Institute of Finance.

Robert W. Colby is a Chartered Market Technician (CMT), an accreditation granted by the CMT Association after demonstrating professional competence and ethics over many years. Robert has been a member since 1980. He also supports The Technical Analysis Educational Foundation, which works to have technical analysis included in the curriculum of major business schools.

"Robert W. Colby is America's foremost authority on testing market indicators."

— Bill Meridian, top-ranked investment analyst and international fund manager, www.billmeridian.com

{kind=link}

{kind=link}